CIAO DATE: 11/2008

A publication of:

The European Institute

Looking beyond the current turmoil in global capital markets, that long-running subject – what outlook for the dollar? – seems likely to involve further decline in its value against the euro and other major currencies. There is scant evidence of willingness on the part of U.S. political and monetary leaders, today’s or tomorrow’s, to do what is necessary to make the dollar fundamentally stronger. Indeed, American policy-makers have powerful reasons to let the dollar depreciate over time, shifting the cost to the rest of the world of U.S. international borrowing to cover shortcomings in economic policies pursued by Washington.

Looking beyond the current turmoil in global capital markets, that long-running subject - what outlook for the dollar? - seems likely to involve further decline in its value against the euro and other major currencies. There is scant evidence of willingness on the part of U.S. political and monetary leaders, today's or tomorrow's, to do what is necessary to make the dollar fundamentally stronger. Indeed, American policy-makers have powerful reasons to let the dollar depreciate over time, shifting the cost to the rest of the world of U.S. international borrowing to cover shortcomings in economic policies pursued by Washington.

In addition, this "benign neglect," to put it euphemistically, coincided with the Bush administration's aversion to using regulatory tools that might have provided timely transparence about some new financial instruments and averted some of the current turbulence in markets. These U.S. policies have deepened doubts about the long-run reliability of the dollar as a store of value.

Ironically, the factor most likely to prop up the dollar's exchange rate would be international disasters that cause foreign capital to flee to the United States. Such a shift back to the United States would probably prove temporary, and the more significant result of any severe crisis would be to further shake international faith in the solidity of financial institutions. A poll published in January 2008 for the annual Davos meeting on world economics showed a prevailing view (60 percent of respondents) that central banks have lost control of the situation they are supposed to be managing. And the United States is certainly not alone in being singled out: the leading French bank, Société Générale, has blamed its recent staggering loss of $7 billion on a rogue individual in its trading department, but this has still shaken confidence in the bank and its supervisory system.

Despite these European policy mistakes, a larger reproach can be addressed to Washington about sowing systemic problems. These stem largely from the hands-off, laissez-faire attitude of the Bush administration toward markets. In practice, this has meant a U.S. aversion to using regulatory tools that could have insisted on adequate transparency and timely accountability about new financial instruments and banking practices.

One egregious example is the absence of oversight for the practice of repackaging U.S. subprime mortgages - high-risk loans with little information about credit-worthiness and the degree of risk involved. These complex securities, which became even more opaque when they were bundled into large packages, were misleadingly marketed to investors worldwide.

Similarly, the Federal Reserve has been reluctant to use its regulatory authority and immense influence to preemptively discourage the growth of asset bubbles built on such securities and on excessively-leveraged borrowing. This ideological mindset against regulatory interference with markets alarms international investors, many of whom worry about the foundations of the U.S. banking system. The U.S. central bank's preference for acting after bubbles burst - in this case, frantically cutting interest rates and resorting to emergency measures to shore up the banking system - reduces international confidence in the U.S. financial system and, symptomatically, in the U.S. currency.

Senior European officials have publicly criticized the United States for the international sell-off in securities that started in July 2007 - which they trace to U.S. excesses and lack of regulatory discipline. France's Finance Minister, Christine Lagarde, said on French radio: "We are not in the same situation as the U.S.A. American households can be 100 percent in debt, with floating interest rates. Unemployment in the U.S. is increasing, in France it is decreasing. U.S. economic growth has slowed." Similarly, according to EU Economic and Monetary Affairs Commissioner Joaquin Almunia, "the main reason why the equity markets have this extreme volatile situation these days is the risk of a recession in the U.S.; it's not about a global recession. Big imbalances have been created; have built over the years in the U.S. economy - a big current account deficit, a big fiscal deficit, (and) a lack of savings." And Luxembourg's Prime Minister, Jean-Claude Juncker, said Europe had "warned repeatedly" about "deficiencies" in the U.S. economy. By late January, Europe's most prominent political figures were calling for more transparency among financial institutions, with Britain's Gordon Brown, Germany's Angela Merkel, France's Nicolas Sarkozy and Italy's Romano Prodi joining European Commission President José Manuel Barroso all expressing their concern.

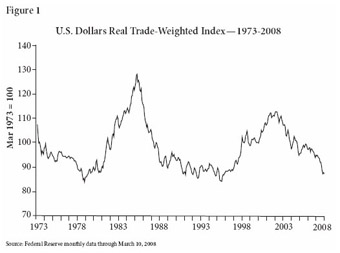

For the dollar, all these factors have undermined the credibility of the official mantra that Washington wants and believes in a strong currency. Seen against this background, the dollar's decline seems to be a long-term trend likely to continue. By mid-March 2008, the dollar hit a historic low of $1.558 against the euro, down 88 percent from its mce_marker.827 high in October 2000. On a real, trade-weighted basis - meaning as evaluated against the currencies of the main U.S. trading partners - the dollar is today at an all-time low since its March 1985 high (see figure 1).

A fundamental factor in the dollar's decline is now-chronic spending by the United States beyond its means. National policies and private sector marketing have emphasized, for decades, consumerism and economic growth even as saving declined. Private consumption rose to 71 percent of gross national product by 2007, up from 61-63 percent between 1960 and 1980; the personal savings rate dropped from 7-8 percent of disposable income through the 1970s to around zero in recent years. This trend was encouraged by the bubbly growth of financial asset prices and house prices, which boosted net household wealth and increased the propensity to spend, not save.

As a result, U.S. imports rose faster than exports and the resulting deficit in trade (and services) has ballooned since the early 1980s. The current account (C/A) - which is the most comprehensive measure of the balance of payments in goods, services and investment flows - showed an estimated deficit of $750 billion in 2007, equal to 5.5 percent of gross domestic product. This signaled a massive shift from the U.S. being a net creditor vis-à-vis the rest of the world (until 1985) to being the world's largest net debtor today. The C/A deficit has been financed by foreigners who acquired dollars by selling products and services to the American market, taking IOU's in the form of dollars because they thought the U.S. was their most profitable market or a good place to invest their savings. Thanks to this confidence, the rise in the C/A deficit of the U.S. was more than off-set by foreign inflows - until recently. In other words, despite its huge external deficit, the U.S. had a breathing space to adapt and adjust policy.

Washington failed to take the opportunity to adopt measures encouraging more domestic saving and more investment in productivity growth in the U.S. These could have boosted economic and job growth and reduced the country's external deficit and dependence on foreign capital. Instead, consumerism has been encouraged by loose fiscal and tax policies since 2001. The Federal Reserve's monetary and credit policies, as well as its reluctance to restrain sharply rising asset prices, contributed to the housing and financial bubbles, plus the resulting wealth effect that encouraged over-consumption and under-saving. Ironically, the resulting economic growth and asset bubbles attracted even more foreign capital. Once the nasty shocks of the implosion of the dot.com equity bubble in 2000 and 9/11 had abated by late 2002, confidence grew rapidly with the Bush tax cuts and very low cost of capital. The result, since 2003, was a sharply reduced risk premium factored into business deals, i.e. there was a decline in the additional return that investors should have demanded to reflect greater risk. All these trends strengthened the Bush administration's attitude of encouraging unfettered adventures in financial markets.

A change that sapped U.S. financial credibility started in 2000-2002 with the wave of corporate scandals at Enron, WorldCom and other major companies. Cases showing widespread corporate book-cooking (what I call "Enronitis") dismayed foreign investors, who slowed their investment in dollar assets. As a result, the dollar, after peaking in October 2000, began to weaken as foreign financing flagged.

Under its then-Chairman Alan Greenspan, the Federal Reserve, citing a variety of factors to justify (or rationalize) its move, lowered its base interest rate to an extraordinary one percent in July 2003, where it remained for a year before climbing back to 5.25 percent. Even then, the effective cost of capital remained low (in light of inflation rates at that time), and credit expansion was aided by rapid international growth of money and credit availability. The Fed started to tighten rates in 2004, but it was too late to restore international confidence: foreign financing of the U.S. external deficit declined, automatically putting downward pressure on the dollar (and causing foreign investors to want even fewer dollars). The euro's share of global reserves rose steadily to roughly 25 percent today - a level that is somewhat more than the total of its original component currencies. While global investors are under no illusions that the 15-country euro-zone economy is as dynamic as that of the United States, the euro is increasingly seen as a reasonably safe diversification for their foreign-exchange reserves, especially given the dollar's fundamental problems. In this situation, an aggravating factor has been Wall Street's propagation of exponentially more complex new financial products - products based on what are called "derivatives" - throughout world financial markets since 2003. These new instruments involved "securitization" and "collateralization," which meant that investment banks bundled individual debt instruments (mortgages, for example) into new, higher-yielding securities. These were given inflated credit ratings (by compliant debt rating agencies beholden to their investment bank clients) that helped persuade investors around the world to buy such securities despite their complexity. Securitization and collateralization were supposed to devolve the final risk from a relatively few mortgage lenders and investment banks to many "final" investors. The reality proved quite different because so much of the new paper really was "subprime," based on "subprime" borrowers liable to default when interest rates rose.

Although warned by domestic and international regulatory authorities, the Greenspan Fed refused to use its regulatory authority to restrain such practices. This benign neglect became egregious as the "securitized" mortgage securities began being used as collateral for more borrowing, at astonishingly high "leverage ratios;" as much more money could be borrowed by hedge funds or private equity group using subprime mortgage-based paper or similar securities as collateral.

As the expansion of credit, and profits, assumed tsunami proportions, the aversion to risk seemed to melt away in the United States and, to a significant degree, in Europe. U.S. political and monetary authorities, mesmerized by the spectacular deals engineered by hedge funds and private equity funds using the cheap capital and new financial engineering, defended the phenomenon, insisting that the wider distribution of risk justified the accelerating expansion. The conservative consensus in Washington continued to insist: no constraints on such successful market strategies.

Repeatedly, the Bank of International Settlements (BIS) in Basel, Switzerland (which brings together most of the world's main central banks, including the Federal Reserve) warned that the gross value of over-the-counter (i.e. unregulated) derivative instruments was growing very rapidly. By autumn 2007, the gross amount of outstanding derivatives exceeded world GDP by a factor of five. But BIS warnings were repeatedly dismissed by Washington.

The fears voiced by the BIS were confirmed by the emergence in the past few years of yet another new derivative instrument: credit default swaps (CDS). These were designed to insure the buyer of corporate debt instruments against default by that corporation by repackaging to spread the risk. The unregulated market for these bilateral, unregulated contracts quickly mushroomed to an estimated $45 trillion today. This showed that market participants were worried about the deteriorating creditworthiness of major corporations and financial institutions, but no regulatory curbs were forthcoming.

Despite the BIS warnings and the rapid growth of CDS, U.S. regulators, mandated by law (usually after previous market disasters and/or scandals) to monitor potential market problems, were ordered by their political masters to "go easy" on enforcing financial and corporate compliance in the interest of letting market forces "work." A blind eye was turned to predatory and risky financial tactics used by mortgage and commercial lenders, hedge funds, private equity groups and the proprietary investment arms of major investment banks.

The alarm should have come when the Fed started raising interest rates in June 2004. Market players realized that subprime mortgage-based securities were at risk since initially low "teaser" mortgage rates would have to be reset substantially higher, making it difficult for low-income borrowers to service their debt. The mortgage "resets" started in 2006 and foreclosures accelerated strongly in 2007, causing the value of the new securities supposedly backed by the subprime mortgages to fall precipitously.

Markets were stunned as evidence quickly emerged of how many of the world's financial portfolios had been contaminated by the toxic paper. Led by U.S. financial institutions' aggressive global marketing, the "securitized" and highly-rated subprime-based securities had been sold around the world. Financial institutions in many countries owned securities that they could no longer price and therefore could no longer sell.

Starting in late July 2007, the subprime crisis caused key financial markets to tumble like dominos: mortgages, commercial paper, money markets, municipal bond insurers. Write-downs of portfolio values continue to mount, with no end in sight for banks and other financial institutions until the wave of subprime resets ends in spring 2009. Worst of all, a paralysis of the interbank market emerged from the continuing difficulties in pricing subprime and other "securitized" and "collateralized" securities.

Because these assets (or, indeed, liabilities) cannot be measured accurately, there was a loss of confidence between the world's largest banks, and starting in the summer of 2007 key banks in financial capitals became reluctant to lend to each other on normal market terms. Despite aggressive injections of liquidity by the Fed, the European Central Bank (ECB) and other central banks, sometimes on a coordinated transatlantic basis, the "interbank market" remains distorted and is a major factor in the ongoing credit crunch. This, in turn, affects the availability of capital to private businesses in the U.S., Europe and elsewhere, and is a major reason for fearing that economic growth could slow into recession.

Stuck with securities that they cannot evaluate or sell, major U.S., European and Asian banks are struggling to boost their core capital (to comply with government-mandated "solvency ratios" of capital to debt) in order to continue doing business. This means accepting major new outside shareholders, such as Sovereign Wealth Funds (SWFs), pools of investment capital with an estimated $3 trillion managed by governments, including China, Russia, Abu Dhabi, Singapore, Kuwait, Saudi Arabia and Norway. So far, these SWFs, which are non-accountable and unregulated, appear to be taking advantage of fire-sale U.S. asset prices to buy shareholdings in key financial institutions for investment, not political, reasons. But as Russian hardball tactics with its energy clients illustrate, politics may influence how some SWFs manage these investments in key U.S. financial institutions in the future.

U.S. policymakers and regulators, very belatedly, moved in the spring of 2008 to ensure that markets function (and to avoid a recession in a presidential election year). Secretary of the Treasury Henry Paulson organized a modest program to freeze some subprime mortgages, the Fed, now chaired by Ben Bernanke, slashed interest rates and implemented new facilities for financing the banking system (but said nothing about increased regulatory surveillance of innovative financial engineering). The White House and Congress (in an exception to the gridlock in Washington) agreed in late January 2008 on a plan for tax rebates and other budgetary stimuli totaling about $156 billion, equal to over one percent of GDP. New York state's insurance regulator met with banks to devise a plan to bail out the corporate insurers of over $2 trillion of municipal bonds - insurance firms whose own credit ratings and capacity to make good their insurance of normally blue chip municipal bonds were undermined by the subprime crisis.

Despite these rescue efforts by "Bush & Bernanke," there will likely be further financial and economic problems this year. This means the Fed will have to cut interest rates further to keep the payments system, markets and economy functioning. There had been speculation that the global economy had grown so strong that prosperity was "decoupled" from events in the United States. Nevertheless, the still-rapid but slowing economic growth in China, India, Brazil and other developing countries seems unlikely to offset a significant slowdown in the U.S., Europe and Japan (which together account for two-thirds of world GDP). As things stand, a recession in the U.S. and Europe would expose even more problems in the banking and financial structure because of the still unknown extent of securitized, collateralized and overleveraged derivative securities throughout the global system.

As systemic risks persist, the flight to safety leads again - ironically - to U.S. Treasury bonds (at least in the short run) and other dollar investments. As a weakening dollar lowers the prices of U.S. companies, sovereign wealth funds will invest more in major U.S. banks and companies - unless this recycling process is hindered by a political backlash among Americans against the specter of "foreign takeovers."

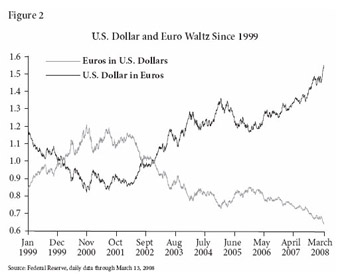

As the dollar declines, U.S. assets will attract foreign investors with strong currencies (or dollars they want to spend down), especially if Washington acts vigorously to stabilize the banking and financial system and insists on more transparency and regulatory surveillance in U.S. markets. Even then, the dollar's long term future seems likely to continue downward: U.S. political and financial leaders will be tempted to repay the United States' huge external debt in depreciated dollars (see figure 2). There is scant domestic political fallout: Few Americans will feel sorry for foreign investors who find the dollar an unreliable place for their savings. (Japanese who invested their export earnings in dollars in the 1980s had lost 42 percent of their holdings because of the dollar's depreciation against the yen by 2007.) But the investment flows to the U.S. will be accompanied by a new readiness for countries with surpluses to put a larger share of their "disposable funds" into investments in non-dollar currencies, notably the euro.

The dollar might be bounced out of its trend downward by a foreign disaster such as a political rupture in the EU or the collapse of the euro, a new Japanese depression, a Russian energy embargo on Europe, turmoil in China or a new oil-price shock. But waiting for bad things to happen abroad is not a solution to America's dollar problem. In the long-run, that problem has created a consensus among many economists, which few dare say publicly - that the United States will pursue a "default-in-slow-motion," reneging on its foreign debt de facto by acquiescing in dollar depreciation and U.S. inflation. ?

J. Paul Horne is an independent international market economist who was a managing director and international economist at Smith Barney/Citigroup based in Europe.

{kind=link}

{kind=link}